2007/2008 Financial Crisis: Financial Industry & Government E-Mails

$4.50

Description

Financial Crisis of 2008: Key Events and Figures

- September 9, 2004: Angelo Mozilo, Chairman and CEO of Countrywide Financial, emails Stan Kurland and Keith McLaughlin regarding “Subprime Residuals.” (Details of the content are not provided in the excerpt).

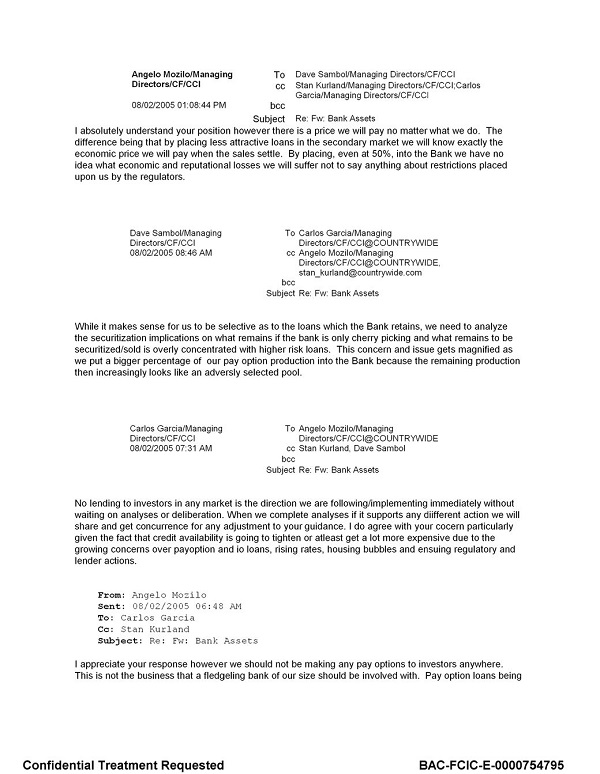

- August 2, 2005: Angelo Mozilo emails senior management at Countrywide Financial, expressing concern that certain “pay option loans” marketed to investors could bring “financial and reputational catastrophe.” He insists Countrywide should not market these speculative loans to investors and highlights issues with borrower quality and abuse by third-party originators.

- February 28, 2006: Gene Park, Managing Director of Financial Products at AIG, emails Joe Cassano, an AIG Financial Products officer, outlining AIG’s decision to stop writing credit default swaps on super-senior tranches of CDOs.

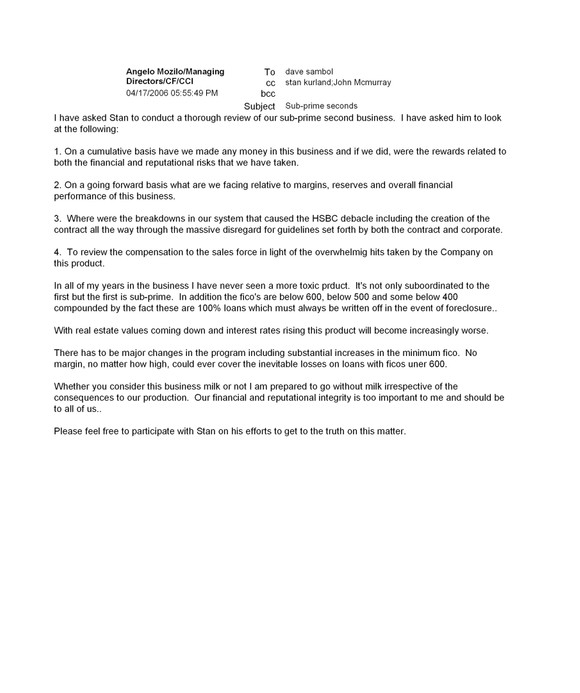

- April 17, 2006: Angelo Mozilo emails David Sambol, President and COO of Countrywide Financial, describing a specific “sub-prime seconds” loan product as the “most toxic ” he had ever seen in his years in the business.

- June 2006 (referenced in November 3, 2007 email): Richard Bowen, Chief Business Underwriter at Citigroup, begins to observe that up to 60% of the mortgages purchased by CitiFinancial significantly fall short of the company’s guidelines.

- March 30, 2007 – April 22, 2007: Emails exchanged between Matthew Tannin and Steven Van Solkema, and Matthew Tannin and Ralph Cioffi at Bear Stearns (content not detailed in the excerpt). These occur in the lead-up to Bear Stearns’ difficulties.

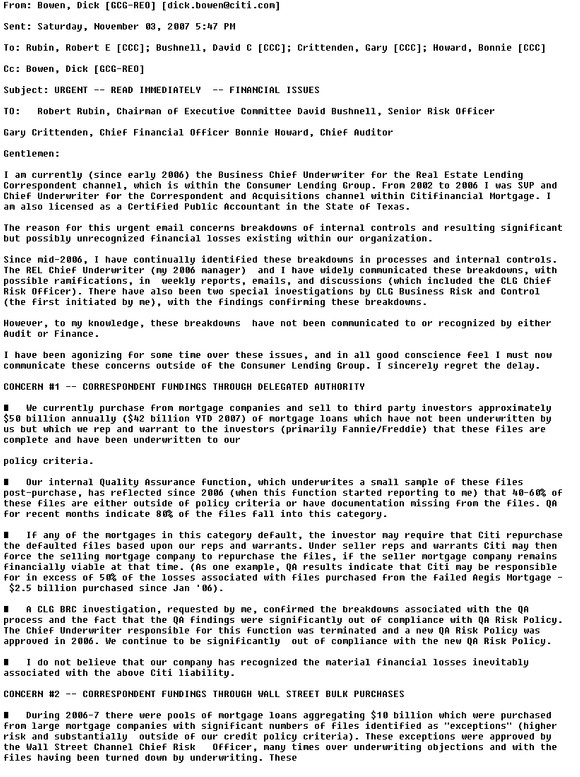

- November 3, 2007: Richard Bowen emails Robert Rubin and other top Citigroup executives with the subject line “URGENT—READ IMMEDIATELY,” detailing the significant issues with loan quality he has observed within CitiFinancial. He had previously attempted to raise these concerns through other channels.

- Early 2008 (referenced in March 7, 2008 email): Treasury Undersecretary Robert Steel has “encouraging” conversations with Senator Richard Shelby and Representative Barney Frank regarding potential GSE reform legislation and capital relief for Fannie Mae. Steel intends to speak with Senator Christopher Dodd.

- March 7, 2008: Daniel Mudd, CEO of Fannie Mae, emails Robert Levin, Fannie Mae’s chief business officer, suggesting that the 30% capital surplus requirement might be reduced without any “trade.” Mudd proposes to Robert Steel that if regulators eliminate a surcharge, Fannie Mae would agree to raise new capital, viewing it as an “easier trade.” He believes the government needs the GSEs to support the mortgage market.

- June 12, 2008: Thomas Fontana, head of risk management in Citigroup’s global financial institutions group, emails Christopher M. Foskett at Citigroup concerning Lehman Brothers (content not detailed in the excerpt).

- September 8, 2008 (referenced in September 9 email): The precarious financial situation of Lehman Brothers becomes increasingly clear. The New York Federal Reserve is informed that Lehman’s tri-party repo exposure is roughly $200 billion, significantly higher than Bear Stearns’ exposure before its collapse. Lehman is trying to secure an investment from Korea Development Bank.

- September 9, 2008: News breaks that the potential investment from Korea Development Bank in Lehman Brothers will not materialize. Lehman’s shares plummet by 55%. At 5:20 p.m., Treasury Chief of Staff Jim Wilkinson emails Michelle Davis expressing his opposition to a government bailout of Lehman Brothers due to anticipated negative press.

- September 11, 2008: An email at 8:26 a.m. from Susan McCabe, a Goldman Sachs executive, to William Dudley, Gustavo Suarez, and Chris Burke at the Federal Reserve Board indicates a highly negative outlook for the day, stating, “It is not pretty, This is getting pretty scary and ugly again…. They [Lehman] have much.” This day is marked by many as the point where Lehman Brothers’ bankruptcy became inevitable.

Cast of Characters and Brief Bios

- Angelo Mozilo: Chairman of the Board and Chief Executive Officer of Countrywide Financial. His emails reveal internal concerns about the risks associated with subprime and pay option loans, even while the company was actively originating and selling these products.

- Stan Kurland: Mentioned as a recipient of an email from Angelo Mozilo on September 9, 2004, at Countrywide Financial. His specific role is not detailed in the excerpt.

- Keith McLaughlin: Mentioned as a recipient of an email from Angelo Mozilo on September 9, 2004, at Countrywide Financial. His specific role is not detailed in the excerpt.

- Carlos Garcia: CEO of Countrywide Bank. He received an email from Angelo Mozilo in August 2005 regarding concerns about pay option loans.

- Gene Park: Managing Director of Financial Products at American International Group (AIG). He sent an email in February 2006 outlining AIG’s decision to cease writing credit default swaps on super-senior CDO tranches.

- Joe Cassano: An officer within AIG Financial Products. He was the recipient of Gene Park’s February 2006 email regarding CDOs.

- David Sambol: President and Chief Operating Officer (COO) of Countrywide Financial. He received Angelo Mozilo’s April 2006 email describing a subprime product as “toxic.”

- Matthew Tannin: Senior Managing Director at Bear Stearns. He exchanged emails with Steven Van Solkema and Ralph Cioffi in March and April 2007, preceding Bear Stearns’ difficulties.

- Steven Van Solkema: Credit analyst at Bear Stearns. He received an email from Matthew Tannin in March 2007.

- Ralph Cioffi: Hedge fund manager at Bear Stearns. He received an email from Matthew Tannin in April 2007.

- Robert Steel: Treasury Undersecretary. He had discussions with Senators and Representatives in early 2008 regarding potential support for Fannie Mae and intended to speak with Senator Dodd.

- Daniel Mudd: Chief Executive Officer (CEO) of Fannie Mae. He engaged in email discussions in March 2008 regarding Fannie Mae’s capital requirements and potential government support.

- Richard Shelby: Ranking member of the Senate Committee on Banking, Housing, and Urban Affairs. He had “encouraging” conversations with Robert Steel regarding GSE reform.

- Barney Frank: Chairman of the House Financial Services Committee. He also had “encouraging” conversations with Robert Steel about GSE reform.

- Christopher Dodd: Chairman of the Senate Banking Committee. Robert Steel intended to speak with him regarding GSE issues.

- Robert Levin: Chief Business Officer at Fannie Mae. He was part of the email exchange with Daniel Mudd in March 2008 concerning capital requirements.

- Richard Bowen: Chief Business Underwriter at Citigroup. He raised significant concerns internally about the quality of mortgages being purchased by CitiFinancial, including sending an urgent email to Robert Rubin in November 2007.

- Robert Rubin: Chairman of Citigroup. He was the recipient of Richard Bowen’s urgent email in November 2007 detailing concerns about loan quality.

- Thomas Fontana: Head of risk management in Citigroup’s global financial institutions group. He sent an email to Christopher M. Foskett in June 2008 concerning Lehman Brothers.

- Christopher M. Foskett: An individual at Citigroup who received an email from Thomas Fontana in June 2008 regarding Lehman Brothers. His specific role is not detailed in the excerpt.

- Jim Wilkinson: Treasury Chief of Staff. He emailed Michelle Davis on September 9, 2008, expressing his opposition to a potential government bailout of Lehman Brothers.

- Michelle Davis: Assistant Secretary for Public Affairs at the Treasury Department. She received Jim Wilkinson’s email regarding Lehman Brothers on September 9, 2008.

- Susan McCabe: A Goldman Sachs executive. She sent an email to individuals at the Federal Reserve Board on the morning of September 11, 2008, expressing a dire outlook related to Lehman Brothers.

- William Dudley: Individual at the Federal Reserve Board who received Susan McCabe’s email on September 11, 2008.

- Gustavo Suarez: Individual at the Federal Reserve Board who received Susan McCabe’s email on September 11, 2008.

- Chris Burke: Individual at the Federal Reserve Board who received Susan McCabe’s email on September 11, 2008.

2007/2008 Financial Crisis: Financial Industry & Government E-Mails

A collection of 806 pages of E-Mails collected by the Financial Crisis Inquiry Commission related to its investigation of the financial crisis of circa 2007. The E-Mails date from 2001 to 2011. In the wake of the most significant financial crisis since the Great Depression, President Barack Obama signed into law the Fraud Enforcement and Recovery Act (Public Law 111-21) that established the Financial Crisis Inquiry Commission to “examine the causes, domestic and global, of the current financial and economic crisis in the United States.” The Commission used the authority it was given to issue subpoenas to compel the production of documents, but in the vast majority of instances, companies and individuals voluntarily cooperated with the inquiry.

These documents were part of its inquiry into institutions that included American International Group (AIG), Bear Stearns, Citigroup, Countrywide Financial, Fannie Mae, Goldman Sachs, Lehman Brothers, Merrill Lynch, Moody’s, and Wachovia. Public institutions covered include the Federal Deposit Insurance Corporation, the Federal Reserve Board, the Federal Reserve Bank of New York, the Department of Housing and Urban Development, the Office of the Comptroller of the Currency, the Office of Federal Housing Enterprise Oversight (and its successor, the Federal Housing Finance Agency), the Office of Thrift Supervision, the Securities and Exchange Commission, and the Treasury Department.

Highlights from this collection

September 9, 2004 – E-mail from Countrywide Financial chairman of the board and chief executive officer Angelo Mozilo to Stan Kurland and Keith McLaughlin, subject: Subprime Residuals

August 2, 2005 – E-mail from Countrywide Financial chairman of the board and chief executive officer Angelo Mozilo to senior management

Mozilo emailed senior management that a section of their loans could bring “financial and reputational catastrophe.” Countrywide should not market them to investors, he insisted. “Pay option loans being used by investors is a pure commercial spec[ulation] loan and not the traditional home loan that we have successfully managed throughout our history,” Mozilo wrote to Carlos Garcia, CEO of Countrywide Bank. Speculative investors “should go to Chase or Wells not us. It is also important for you and your team to understand from my point of view that there is nothing intrinsically wrong with pay options loans themselves, the problem is the quality of borrowers who are being offered the product and the abuse by third party originators. . . . [I]f you are unable to find sufficient product then slow down the growth of the Bank for the time being.”

February 28, 2006 – E-Mail from AIG Managing Director of Financial Products Gene Park to AIG Financial Products officer Joe Cassano, Subject: CDO of ABS Approach Going Forward – Message to the

Dealer Community

This e-mail marks AIG decision to stop writing credit default swaps on super-senior tranches of CDO’S.

April 17, 2006 – Angelo Mozilo, email to David Sambol, April 17, 2006, subject: sub-prime seconds.

Countrywide’s Mozilo to Countrywide’s President and COO David Sambol describes one of the loan products his firm was originating.“In all my years in the business I have never seen a more toxic ,” he wrote in an internal email.

March 30, 2007 – E-mail from Bear Stearns Senior Managing Director Matthew Tannin to Bear Stearns credit analyst Steven Van Solkema.

April 22, 2007 – E-mail from Bear Stearns Senior Managing Director Matthew Tannin to Bear Stearns hedge fund manager Ralph Cioffi.

In the days leading up to the Bear Stearns meltdown, Treasury undersecretary Robert Steel informed Fannie Mae CEO Daniel Mudd that he had “encouraging” conversations with Senator Richard Shelby, the ranking member of the Senate Committee on Banking, Housing, and Urban Affairs, and Representative Barney Frank, chairman of the House Financial Services Committee, about the possibility of government- sponsored enterprise (GSE) reform legislation and capital relief for the GSEs. Steel intended to speak with Senate Banking Committee Chairman Christopher Dodd. Mudd was confident that the government desperately needed the GSEs to back up the mortgage market, so Mudd proposed an “easier trade.” Mudd proposed that if regulators would eliminate the surcharge, Fannie Mae would agree to raise new capital. Also in this March 7, 2008 email to Fannie chief business officer

Robert Levin, Mudd suggested that the 30% capital surplus requirement might be reduced without any trade: “It’s a time game.. whether they need us more… or if we hit the capital wall first. Be cool.”

November 3, 2007 – E-mail from Dick Bowen to Citigroup Chairman Robert Rubin, and other top Citigroup executives, concerning unrecognized financial loses.

Richard Bowen was chief business underwriter at Citigroup. He oversaw loan quality for over $90 billion a year of mortgages underwritten and purchased by CitiFinancial. Bowen says that in June 2006 he came to see that up to sixty-percent of the loans that were being purchased by CitiFinancial had seriously fell short of Citi’s guidelines. Citi could be forced to buy back loans it sold to other institutions if the borrowers defaulted.

In an interview with staff members of the Financial Crisis Inquiry Commission, Bowen said that he attempted to inform his superiors of the danger through email, weekly reports, committee presentations, and discussions. Unsatisfied with the actions taken, he went to the highest level at Citigroup with the e-mail below. In an e-mail sent to Robert Rubin with the subject “URGENT—READ IMMEDIATELY,” Bowen spelled out the trouble he discovered.

June 12, 2008 – E-mail from Thomas Fontana, head of risk management in Citigroup’s global financial institutions group, to Citigroup’s Christopher M. Foskett, concerning Lehman.

September 9, 2008 – E-mail from Treasury Chief of Staff Jim Wilkinson to Michelle Davis, assistant secretary for public affairs at Treasury, expressing his distaste for government assistance to Lehman.

By September 8th, 2008 the fact that Lehman was moribund became even clearer. The New Federal Reserve Bank was informed that Lehman’s tri-party repo exposure was at roughly $200 billion. Before its collapse Bear Stearns’s exposure had been at most $80 billion. Lehman was working on an investment by Korea Development Bank to raise capital.

On September 9th news broke that there would be no investment from Korea Development Bank. Lehman shares fell by 55 percent.

Treasury Department Chief of Staff Jim Wilkinson at 5:20 p.m emailed Michelle Davis, the assistant secretary for public affairs at Treasury, to express his distaste for government assistance: “We need to talk… I just can’t stomach us bailing out lehman… Will be horrible in the press don’t u think.”

September 11, 2008 – Federal Reserve Bank E-mail from Susan McCabe to William Dudley, Gustavo Suarez and Chris Burke, “this is shaping up as going to be a rough day.”

September 11, 2008 is marked as the day by many that the Lehman Brothers bankruptcy was set in stone.

On Thursday September 11, an email time-stamped 8:26 a.m. from Susan Mc-Cabe, a Goldman Sachs executive, to William Dudley, Gustavo Suarez and Chris Burke at the Federal Reserve Board set the tone for the day: “It is not pretty, This is getting pretty scary and ugly again…. They [Lehman] have much.

Related products

-

Watergate Break-in Investigation FBI Files

$19.50 Add to Cart -

Journal of the Congress of the Confederate States of America 1861-1865

$19.50 Add to Cart -

Civil War: Frank Leslie’s Weekly Illustrated Newspaper (1860-1865)

$19.50 Add to Cart -

Watergate: Congressional hearings, reports, exhibits, and transcripts

$19.50 Add to Cart